If you’ve resolved to improve your finances or even prepare to purchase a home, in the coming months, you’ll need a solid plan to set yourself up for success. Here are three ways to help you better manage your money in 2018.

Start a budget. A budget is just a plan for every dollar you earn, and there are a lot of tools to help you strategize. Start with your monthly after-tax income and then list your monthly expenses, including set payments such as the rent or mortgage as well as those that vary, like utilities, credit cards and gas. Don’t forget extras, such as streaming subscriptions, or expenses like car insurance that only crop up a few times a year.

Pay down debt. Your budgeting process should have identified your debts, so now you need to focus on repayment. Two common methods can help with this: There’s the avalanche approach, which prioritizes your highest-interest debt, and then there’s the snowball method, which focuses on paying back your smallest debts first. While the avalanche method saves you the most money in the long run, some say the small wins of the snowball approach can help keep you on track.

Build an emergency fund. Having three to six months’ worth of savings can help you avoid relying on high-interest credit cards in the event of a job loss or other emergency. Cutting costs is an obvious first step in unearthing those savings, so try to make more meals at home, take advantage of loyalty programs and avoid small, frequent purchases like morning coffee. Once you’ve saved a little bit, make the most of these funds by placing them where they’ll offer better returns than a traditional savings account.

Getting your finances in order isn’t always fun or easy, but following the guidelines above can help you get off to a good start.

Would you like to see how close you are to home ownership? Call us today at 208.895.9944

If you’ve been sitting on the fence about selling your home, it might just be time to hop off. Now. To put it in other terms: 2017 is poised to be the year of the home seller, real estate experts say. So what are you waiting for?

A combination of factors is coming together to make 2017 a prime seller’s market for most of the nation. Here are 3 upgrades that will give your home an extra edge over the competition, boost your potential list price, and where you will see the best return on your investment.

1 – Yard / Curb Appeal

You only have one chance at a first impression. If a buyer drives up to your home and sees the yard is overgrown, toys strewn about, and the mulch is dried and lost its color, they may start to formulate impressions of how the interior is being maintained.

There are entire shows based on renovating backyards and curb appeal. This should speak to you as a homeowner. Buyers are interested in and put value behind outdoor entertaining space!

If you have it in your budget, hire a professional landscaper to help give your yard a facelift.

Don’t have it in the budget to hire a professional? You’re in luck, there are several things you can do on your own: keep the yard free of debris, trim the grass, trees, and shrubs, add fresh mulch to flower beds, and ensure the sidewalks are swept clean.

A poor yard could result in up to a 10% loss of value in your home.

2 – Outdoor Upgrades

Outdoor upgrades are great because they are generally the cheapest improvements and have the greatest return on investment. These outdoor improvements are installing new windows, updating the garage door, and installing a new front door.

On average, the return on investment for these kind of upgrades can be as high as 72%! That is nothing to shake a stick at.

3 – Adding another Bathroom

For those of you who have ever had to share one bathroom with a large family, or in my personal case, just my husband, you know how important multiple bathrooms are.

Did you know that adding even a half bath to your home could increase your property value by 10.5%? A full bathroom could give you up to 20%!

Adding some more bathroom (pun intended) to your home could pay off in dividends.

Have questions on how to improve the value of your home and get it ready for the open market? Give our office a call at (208) 895-9944

There is no denial that we are working with one of the hottest real estate markets where the supply is low and demand is high. Many buyers are finding themselves in a bidding war, with multiple offers pushing prices higher and higher.

Add low mortgage rates into the mix, and buying a home can feel like you’re competing in a fierce battle to win the house you love. It’s certainly easy to get discouraged if you’re edged out multiple times when trying to buy a home.

The best move you can make before writing any offers is to hire an experienced, professional real estate agent. Having someone on your side who knows your local market thoroughly — and can guide you through these sometimes tough negotiations — means you’ve got heavy backup when you enter a bidding war.

Here are some strategies to help you come out on top.

Get a Pre-Approval Letter from a Lender

Getting pre-qualified, which merely confirms your income and how much a bank might be willing to lend you based on your credit profile, isn’t the same ashaving preapproval for a specific purchase offer.

Watch this quick video on the difference of pre-qualified vs. pre-approval

You can up your chances of beating out other buyers by including a letter from your bank stating that your lender has underwritten your application and it’s simply pending appraisal.

Skyline Realty suggests submitting all of your financing documentation to your lender before looking at homes and certainly before writing any offers. That way you can pounce quickly when you find the home you want, and avoid the stress of submitting preapproval paperwork and writing an offer at the same time.

Use an Escalation Cause

If you’re in a multiple-bid situation, you can strengthen your offer by using what’s called an escalation clause. It’s essentially a contract addendum that states you’re willing to increase your offer incrementally up to a certain limit if other offers come in that match or top your initial bid.

For example, say the seller’s asking price is $200,000. Your real estate agent would write your offer to state: “My initial bid is $200,000 with an escalation of $2,000 over competing offers up to $210,000,” or something to that effect. If another bidder offered more than $210,000, however, you’d be out of the running.

An escalation clause is a smart strategy that shows strong interest, but it’s important to stay within your budget and be willing to walk away if bidding goes beyond your limit.

You can also allow your bid to be held as a backup offer for up to 20 days if the higher bidder makes an irrational offer and doesn’t deliver earnest money or stops payment.

Limit Contingencies

Sellers have the upper hand in a multiple-bid situation, and they want offers that are clean and concise. If you know other bids are coming in and you really want a home, avoid putting in too many contingencies or making too many demands.

Don’t include things like needing to wait for a spouse or partner’s approval, asking the seller to purchase a home warranty or requesting that the seller leaves or repairs certain items. You also don’t want to ask the seller to pay your closing costs; find an affordable attorney or title company to represent you. Having too many of these items in your contract will make it likely that a seller tells you ‘no’ over another offer.

Be Flexible On Close Date

Let’s say someone outbids you by a few thousand dollars, but you’re willing to give the seller more time to move out. That flexibility can make you the front-runner in a multiple-bid scenario. Extending that courtesy can make your offer more attractive to a seller who might otherwise have to spend more on moving expenses or be crunched for time to find another home. It should be noted that there are limitations on how long a seller can lease back a home based on a buyers loan requirements.

On the other hand, if a home is already vacant, sometimes you can win the seller over by offering to close in a shorter time. Buyers who offer to close quickly can edge out buyers who haven’t been preapproved or have to sell their current home to buy a new one. (Keep in mind, though, that a new regulation known as the TILA-RESPA Integrated Disclosure rule has slowed down closings for some lenders.)

Become ‘Real’

With so much fierce competition out there, it is easy for a seller to view everyone as numbers on paper. Sometimes appealing to the heart can make your offer stand out. That’s why more and more real estate agents are suggesting that buyers write a heartfelt letter to sellers explaining why they want the house.

“I definitely ask my buyers to write a letter and explain how much it would mean to them to get the house,” says Skyline REALTOR® Alexandra Scanlon. “I even have them add a couple of photos of them and their kids or pets. I’ve had selling agents tell me that it was the letter and the complete offer packet that won my clients the listing. We have even had our offer accepted when it was lower than other offers on the table”

Don’t Count Yourself Out After the Bidding War

If you lose a bidding war and the seller chooses another bid, have your agent keep in touch if you’re still interested in the house. If a buyer offered way over the asking price, the deal could fall apart on appraisal or the buyer might be bidding on multiple properties to see which one sticks. The highest offer doesn’t always mean it’s the best one.

Contracts that come in way over asking price have a very high cancellation rate and when that happens, [the seller] loses the momentum of being the new home on the market. That could make your offer attractive again.

Plan Ahead

The homebuying process can feel cutthroat at times, but you’ll be in a better position to win the house you want with a knowledgeable Realtor to help you write a strong, competitive offer that follows these strategies.

You may well lose one or two bidding wars before you win one; it’s almost a rite of passage for homebuyers!

Are you ready to purchase a home and work with a great team? Call us today at (208) 895-9944.

Many people who would like to own homes have fears that prevent them from buying. And rightfully so, as buying a home is usually the largest purchase a person ever makes. If you’re one of these people who is hesitant, take heart – there are simple steps you can take to overcome your fears and become confident that you will make a sound purchase. Here are the top 6 reasons you may be holding off on purchasing a home and how to overcome these hurdles.

1 – Loss in Property Value

The Millennial Generation has been very cautious to take the leap into homeownership after witnessing their parents suffer through the 2008 real estate market crash. Many of these homeowners became underwater (owed more on their loan than the market value) and were forced into foreclosure or short sales.

It is also true that homes can lose their value without a major disaster, such as: the property being in an older neglected neighborhoods and poor city planning by constructing a jail, landfill, or highway nearby.

Although you cannot always predict the housing market there are securities in place and precautions you can take. Lending standards are much higher today than they were in 2008 and sub-prime lending is a thing of the past. This means that banks are only approving mortgages to families that can afford them and for prices that are not overly inflated. Precautions you can take are buying in a low-crime area where the homes are well-kept, primarily owner-occupied and with high-quality schools nearby. You can contact the city government to ask about future development plans in the area you want to buy.

2 – Maintenance Worries

Yes, there is maintenance. If your landlord is completing maintenance (important point: IF), then you will also be paying for that maintenance in increasing rent over the years.

To avoid buying a money pit you should always have a home inspection completed prior to purchasing a home. The home inspection will detail any current or possible future maintenance issues.

Other ways to curb possible maintenance issues are: purchase a home that has been well-maintained, purchase a home that has recently had major components upgraded or replaced (e.g., new roof, new water heater, new plumbing, new electrical), purchase a new home (though new homes sometimes have undiscovered defects, regularly maintain your home to prevent small problems from becoming major repairs.

It is prudent that you consider having an emergency fund set aside for maintenance issues and continue to add to it on a monthly basis.

A final option to consider is purchasing a property, like a condominium, that is within a HOA. Generally, the HOA will take care of the majority of common area maintenance such as: landscaping, roof repair, exterior maintenance, etc…

3 – Mortgage Affordability

Before you take on a mortgage, set up a budget so you know what your existing expenses are and how much money you take home every month. Also, think about new expenses that will come with home ownership, like property taxes, landscaping, water/trash, etc…

Many people wonder how they will afford their mortgage if they lose their job. They also might see that the mortgage payment required to afford a home in their area exceeds what they currently pay in rent. To deal with potential job loss, make sure to have a large emergency fund set aside. You can use this money to continue paying the mortgage if you lose your job.

Something that doesn’t always come to mind when preparing to take on a mortgage is having health insurance in place. Unexpected medical bills are a common source of financial instability. This is something you should consider prior to looking at owning a home.

4 – Finding the Right Mortgage (that you understand)

If you feel that you are not financially sophisticated enough to manage a mortgage, there are two simple remedies to this problem:

First, start educating yourself about how mortgages work, and don’t buy a home until you understand what you’re getting into. There are numerous books, articles and classes available on the subject.

Like finding a deal in real estate, you must find a professional that you can trust. The loan products available are available to almost anyone completing loans. Whether you work with a broker or a direct lender (advantages and disadvantages to both – read the book), find someone that can review your specific situation, your short and long term financial goals, and offer the best options for you.

Second, if you’re still uncertain, get a 15- or 30-year fixed-rate mortgage. These mortgages have withstood the test of time and are the most basic and most foolproof mortgages available.

5 – Not Understanding the Real Estate Process

There are a lot of steps and extra costs that could come as a surprise to first time home buyers. Making the decision to purchase a home and how to plan accordingly can only be successful if you know all the details. Here is a brief overview of the process:

8 – Move In Preparations (Utilities / Change of Address/ Moving Day)

9 – Closing

The right Realtor® will be able to detail this process out to you and also help you navigate along the way.

6 – Not Trusting Real Estate Agents

Yes, the industry has its issues. There are some really, really bad agents out there. However, there are those of us who went into the profession to make it better, to really help home owners and home buyers, and we really, really know our stuff. We are professional, we return calls, we do our homework, we know the neighborhoods like the back of our hands, we see anywhere from 12-50 houses a week (a staggering 3000 homes a year), we drool over MLS (multiple listing data) until wee hours in the morning, and maybe most importantly we believe in the concept of home ownership. If you don’t have an agent you feel you can trust, if you don’t believe they have your back; fire them. Find an agent that supports your goals, places your best interest first, will answer every question with a smile, and addresses every concern before, during, and after the sale.

In summary, caution in any market is prudent and necessary. If you are considering buying a home there must be a reason, an understanding of the reason and a desire to support the goal with true professionals and knowledge. Knowledge is simply smart living. If you have questions or concerns about buying a home contact us.

OK Sellers, we have a little tough love for you today. Now is a great time to sell your home and most homes are sold within the first week of going on the market. However, here are three ways that Sellers are (unintentionally) sabotaging the sale of their home:

– Overbearing Statement Pieces/Paint

While Skyline Realty Boise loves to celebrate our clients’ unique personalities and sense of style, we have to be the voice of reason when it comes to placing your home on the market. When potential buyers are walking through your home it is pertinent to have minimal barriers for the buyers to imagine their furnishings in the home or their family.

A beautiful orange accent wall may compliment your furniture but it would be very distracting for a potential buyer. Another thing to keep in mind is putting away most of your family photos and clearing clutter / oversized furniture.

Keep it neutral and keep it simple!

– Greeting Potential Buyers at the Door

When touring homes with potential buyers there is nothing more awkward than the seller being present! This ties back into allowing the buyers to envision themselves in your home with minimal barriers. When a seller is home the house becomes less of a blank canvas for the buyers and they may concentrate more on the feeling of ‘intruding’ versus the home and how it fits their needs.

If you are worried about the safety of your personal belongings please remember that these potential buyers are accompanied by licensed real estate professionals. Licensed professionals are held to several standards of accountability and how they protect clients/customers.

When you have scheduled showings, make the home available (without you). Go walk the dog!

– Over Pricing Homes

Yes, the market is hot. Yes, it is a seller’s market. Yes, home prices are rising. No, you cannot have any price you dream up! It is so important to stay within the comparable home prices of your neighborhood. Your agent will prepare a Comparative Market Analysis (CMA) of your home and how it stacks up against other homes in your neighborhood that are similar to your home. This tool is vital in selecting the best listing price for your home as it will be most similar to the tools other agents, buyers, and bank appraisers use to determine the value of your home.

If you have the highest priced home (without proper justification) in your neighborhood, you will sell the other homes faster and your home will become what is known as a stale listing.

The longer your home sits on the market the more money you are losing. You will most likely be making more mortgage payments and increasing the chances of list price reductions or paid concessions at closing.

Optimal pricing with be profitable and sell your home quickly.

To find out more information on your home’s value and how to sell it successfully, contact us at (208) 895-9944.

Some homeowners consider trying to sell their home on their own, known in the industry as a For Sale by Owner (FSBO). The popular belief is that by selling your home without an agent you can retain more money by not paying out commissions.

However, according to the National Association of Realtors, “for sale by owner” properties lose 28% of the price they could have gotten if the owner went with an agent (taking commission into account). USA Today did a study and found they really only lost an average of 21%.

Here are four reasons to reconsider your For Sale by Owner:

#1 – Liability

The paperwork involved in selling and buying a home has increased dramatically as industry disclosures and regulations have become mandatory. Are you aware of all the contracts and information that you must provide throughout a transaction? Are you aware that some activities could be illegal even with the best of intentions? This is one of the reasons that the percentage of people FSBOing has dropped from 19% to 9% over the last 20+ years.

#2 – Time

Will you be able to let anyone in during the week to see the property? (if not, fewer offers = less money). Do you have the time to field all the calls, faxes, and inquiries that will come with multiple offers? One missed phone call or fax could kill a deal. You will also need to make time to negotiate with buyers who want the best deal, buyer’s agents who only represent the interest of their client, investors, attorneys, home inspection companies, appraisers, and possibly your bank.

#3 – Exposure

Recent studies have shown that 92% of buyers search online for a home. That is in comparison to only 28% looking at print newspaper ads. Most real estate agents have an internet strategy to promote the sale of your home.

You will get the most money for your home in the first week that it’s on the market (in this market), and the longer it’s on the market, the less money people are willing to offer. If you try the “for sale by owner” approach and then change your approach to work with an agent, you will also have already eliminated the buyers who saw it in the first place, who may have low-balled it thinking you were easy prey, and who are not willing to make a second offer – they’ve moved on.

#4 – More Money

Many homeowners believe that they will save the real estate commission by selling on their own. Realize that the main reason buyers look at FSBOs is because they also believe they can save the real commission. The seller and buyer can’t both save the commission.

Studies have shown that the typical house sold by the homeowner sells for $184,000 while the typical house sold by an agent sells for $230,000. This doesn’t mean that an agent can get $46,000 more for your home as studies have shown that people are more likely to FSBO in markets with lower price points. However, it does show that selling on your own might not make sense.

Before you decide to take on the challenges of selling your house on your own, sit with a real estate professional in your marketplace and see what they have to offer. Click here to see what we can do for you.

Here is to enjoying this beautiful summer! Even with the rising home prices and reduced inventory of the last few months, pending home sales are down from last month, indicating sales will be slower in July and August. This peaking of home sales in July has been the trend since the market bottomed-out in late 2010. This does not mean prices will fall, but the tight market will soften.

Here is a review of the 2016 year-to-date pending home sales in Boise:

January: 1,056 % Change: (baseline number)

February: 1,305 % Change: +23.6%

March: 1,559 % Change: +19.5%

April: 1,722 % Change: +10.5%

May: 1,810 % Change: +5.1%

June: 1,709 % change: -5.9%

The softening of the market could be a good sign for first-time home buyers and possibly investors. Now is a good time to take advantage to lock in a low interest rate for the next 15 to 30 years.

On a final note, to touch on the looming question of, “Are we in another housing bubble?”, the answer is, No!

When we saw prices peak ten years ago, real estate was much less affordable than it is today. Many of the purchases at that time were being made by investors buying their fourth, fifth or tenth properties. A good part of the financing was based on low or no down payment loans with a complete disregard for incomes and credit scores. Today, the majority of the demand is from real buyers who intend on living in the property. To get a home loan- a down payment, credit history, and income are required. Only a small part of real estate purchases are being made by investors.

In its simplest form, real estate market demand is driven by population. In Boise, the population has increased by 9% from 2006 to 2015. In Meridian, Idaho the population has increased by over 50% in the same time frame. That is a lot of new demand.

Whether it is your first home or your fourth, the home buying process can be a little (read: a lot) stressful. Luckily, we live in the information age and there are a plethora of tools available to make the entire experience more personalized and enjoyable. Here are three apps that every buyer should consider using when searching for their next home:

1. A Mortgage Calculator

A mortgage calculator app, such as this free one from Zillow will show you how much home you can afford. This app will also break down your monthly payments to show how much you are paying for loan balance (principal), interest, and taxes. This app is a great tool when you are deciding on a monthly payment that you are comfortable with.

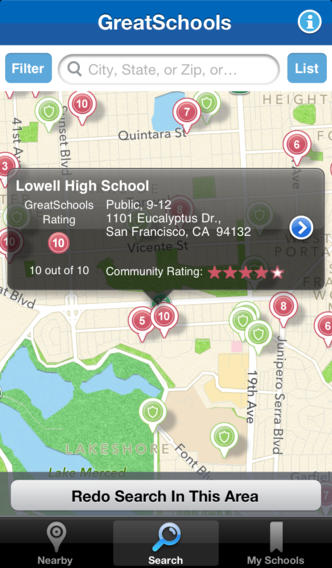

2. GreatSchools Finder

GreatSchools Finder allows the user to view school zones in the neighborhoods that you are looking in. The interactive map also allows you to compare schools K-12 to other schools in the city and state. You will be able to view detailed ratings, reviews, and test scores from the app as well. This tool will assist you in deciding what school is best for your family

3. Better Homes and Gardens ® Real Estate Home Selection Assistant

Home Selection Assistant aims to streamline the process of choosing a home, once you’ve already decided on a few to see. While you’re touring a home, you can use the app to take photos and make notes about the property. Buying a house or condo isn’t a split decision for most, and when looking at tens (or hundreds) of properties their qualities—both positive and negative—can often blend together. The BH&G app is designed to replace your pen, notebook and digital camera, and enhance your memory so you can accurately recall a property when it’s decision time. Plus, with everything stored in your iPhone, you can easily send photos and information to others for input.

Don’t allow home buying to overwhelm you when there are so many available tools to make the process enjoyable. For more information on apps to assist you in your home buying process, call us at (208) 895-9944.